Key Takeaways

- DSCR loans provide income-based financing options for property investors, using rental revenue for loan approval.

- Agents can add value by educating investors on eligibility, documentation, and risk mitigation for DSCR loans.

Despite market volatility, investor demand for DSCR loans is on the rise in 2026—understanding qualification and structure is more essential than ever. If you’re advising investor clients or evaluating alternative financing, having a thorough grasp of DSCR loans is key to setting expectations and ensuring successful outcomes.

What Are DSCR Loans?

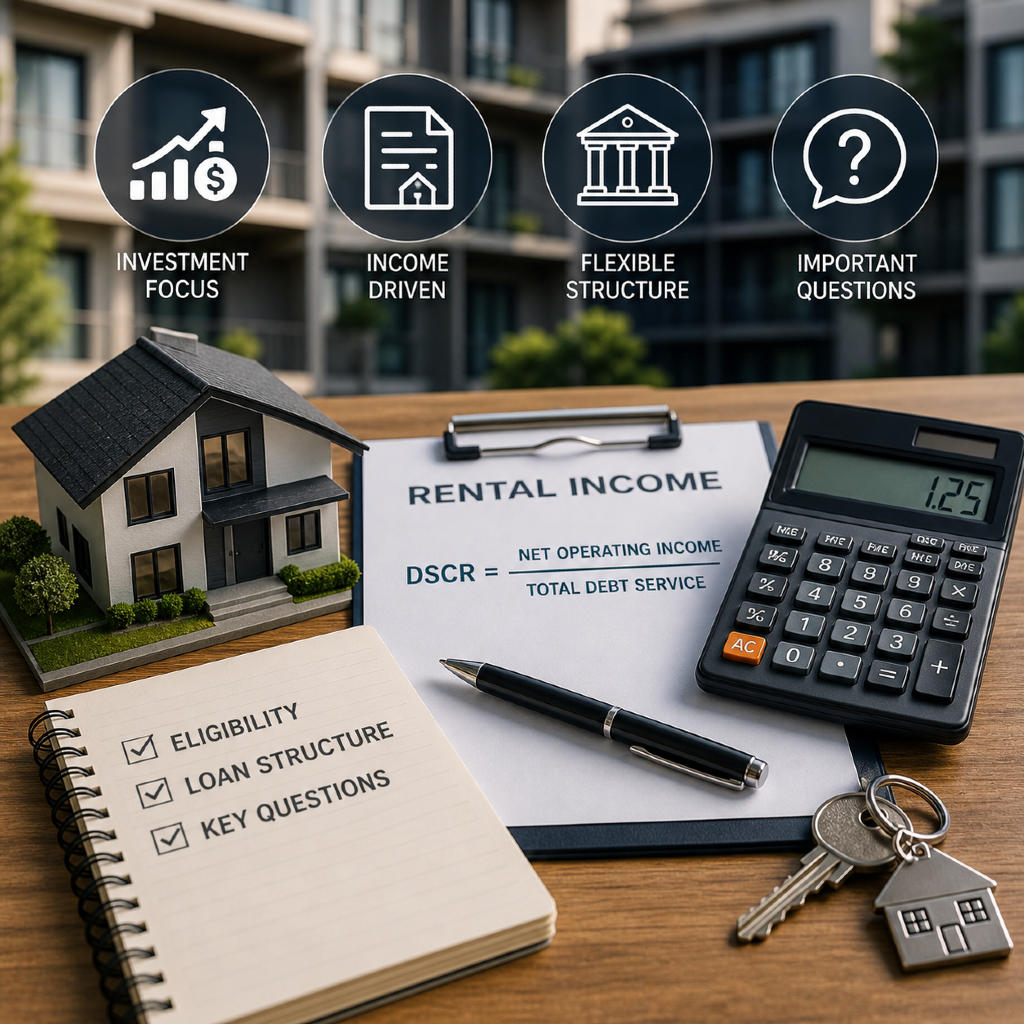

DSCR loan definition

A Debt Service Coverage Ratio (DSCR) loan is a type of real estate financing that evaluates property income—rather than personal income—for approval. The DSCR measures how well a property’s rental or lease income can cover its mortgage payments and related debts.

How these loans work

DSCR loans focus on a property’s actual or projected cash flow, allowing investors to qualify based on the property’s performance instead of tax returns or W-2s. The lender calculates the DSCR by dividing the property’s annual net operating income by its annual debt payments. A higher DSCR indicates a safer risk, with most lenders looking for at least a 1.25 ratio (meaning the income is 125% of the debt obligations).

Who uses DSCR financing

DSCR loans are widely used by real estate investors purchasing or refinancing rental properties. They appeal to those who may not qualify for conventional loans due to unique income sources, high leverage, or a focus on real estate portfolios, including both new and experienced investors.

How Do DSCR Loans Work for Investors?

Income-based qualification

Unlike traditional home loans, DSCR loans typically ignore your personal income. Instead, lenders assess if the property’s rental income can support mortgage payments, taxes, insurance, and HOA fees. This approach is particularly beneficial for full-time investors or those with complex financial profiles.

Property types eligible

DSCR financing is most often used for residential investment properties such as single-family rentals, duplexes, triplexes, or fourplexes. Some programs also allow short-term rentals and small multifamily buildings, provided sufficient rental income can be documented. Commercial properties may qualify, but lender requirements differ.

Loan terms and requirements

Loan terms usually range from 5 to 30 years, with both fixed and adjustable rates. Down payments of 20–30% are common, though lenders may be more flexible if the DSCR is strong. Prepayment penalties, escrow requirements, and reserve funds can apply. Borrowing capacity often links directly to the property’s cash flow—and some lenders set limits on the number of financed properties you can hold.

Who Qualifies for a DSCR Loan?

Eligibility criteria in 2026

As DSCR loans gain popularity in 2026, eligibility standards focus on property performance and investor experience. Typically, lenders look for:

- Solid DSCR ratios (usually 1.25 or higher)

- Documented rental income (leases, market rent reports, or short-term rental history)

- A suitable property appraisal

- Sufficient down payment and closing funds

Common borrower profiles

Investors exploring DSCR loans range from first-time rental owners to seasoned portfolio managers. They’re often:

- Self-employed or have non-traditional income

- Building large rental portfolios

- Seeking to scale their investments without the hurdles of personal income documentation

Credit and income considerations

While DSCR loans focus on property cash flow, most lenders still require a minimum credit score (generally above 660). Personal income may be reviewed, but it’s typically not the deciding factor. Strong asset reserves and a stable rental history can help demonstrate reliability and offset perceived risk.

What Makes DSCR Loans Different?

Investment loan comparison

DSCR loans stand out from other investment property loans because approval relies primarily on rental income performance—not personal income, tax returns, or traditional underwriting templates.

DSCR vs. conventional loans

Conventional loans demand personal proof of income and often rigid debt-to-income ratios. By contrast, DSCR loans streamline the process for self-employed or higher-risk investors, but may have slightly higher rates, lower LTV limits, and unique property eligibility standards.

Non-traditional underwriting explained

Lenders calculate the DSCR to determine if projected rents easily cover mortgage outflows. This approach may let you qualify for more properties—or bigger investments—than possible with a bank statement or W-2 approach. However, you should always compare total costs and long-term flexibility before choosing a loan structure.

What’s Required for DSCR Loan Approval?

Documents investors need

To apply for a DSCR loan, you’ll generally submit:

- Property appraisal

- Purchase contract

- Lease agreements or rental projections

- Operating expense documentation (taxes, insurance, association fees, etc.)

- Down payment account statements and asset verifications

DSCR calculation basics

Lenders compute the DSCR as follows:

DSCR = Annual Net Operating Income (NOI) / Annual Debt Service (loan payments)

A DSCR greater than 1.25 is typically the minimum for approval, though some lenders may accept different thresholds based on the full investment profile.

Typical lender expectations

Expect lenders to scrutinize:

- Rental income verification (leases or market comparables)

- Consistent recent occupancy

- Sufficient cash reserves to handle vacancies or repairs

- Clear property title and no unresolved liens

Lenders may also want to see property management plans or income statements if you own multiple rentals.

What Are the Benefits and Risks?

Key advantages for investors

- Qualification based on property, not individual borrower income

- Greater access for self-employed or portfolio investors

- Possible to scale holdings without numerous personal income checks

Potential drawbacks to consider

- Higher down payments and interest rates than some conventional products

- Tighter property eligibility (not all property types qualify)

- Prepayment penalties or other restrictive loan terms are possible

Mitigating financing risks

You can lower risk by vetting properties for stable rental demand, maintaining cash reserves, and partnering with experienced property managers. Consulting financial and legal professionals before entering complex investments is also recommended.

How Can Agents Advise Investor Clients?

Setting realistic expectations

Educate clients on how DSCR loans differ from standard mortgages. Make it clear that property performance and documentation are crucial, and that not all properties or clients will qualify.

Helping clients prepare applications

Assist clients in gathering accurate rent rolls, expense logs, financial statements, and property management plans. A complete, organized application can speed up loan processing and improve approval odds.

Educating on loan options

Guide investors to compare DSCR loans against other loan types in terms of cost, flexibility, and investment fit. Avoid making promises about approvals or outcomes—focus on helping clients understand their choices and risks.

DSCR Loan FAQs for 2026

Current program changes

Lenders continue evolving DSCR guidelines, often updating minimum DSCR ratios, property standards, or documentation requirements to reflect market trends and regulatory shifts.

Frequently asked investor questions

Common questions include:

- What if my property doesn’t meet DSCR guidelines?

- How quickly can I close with a DSCR loan?

- Are short-term rentals still eligible in 2026?

Emphasize that lender requirements can vary; thorough documentation and preparation are always essential.

Best practices for 2026

Encourage clients to:

- Stay informed on the latest DSCR lender programs

- Review multiple loan offers

- Regularly assess portfolio performance

By maintaining an educational, guidance-focused relationship with your investor clients, you’ll help them make informed, sustainable financing decisions.